To Rent or Not to Rent

For a growing percentage of New Zealanders the answer is no. According to Ministry of Housing & Urban Development (HUD) the rate of home ownership in NZ has dropped from a peak of 73.5% in 1991 to 64.5% in 2018. The proportion of households that are renting has increased from 23% in 1991 to 32% in 2020.

In summary home ownership rates have declined and the proportion of households living in the rental market has increased - more people, including families and older people, are renting for longer, or for life. With this in mind HUD undertook a reform of the Residential Tenancies Act (RTA 1986) in 2020. Reforming the 30 year old RTA was an opportunity to consider whether the law that governs the rental market continues to be a fair and proportionate way to address problems that tenants and landlords may experience with insecure tenure. If you have a property manager great, if not best you have a read of what your obligations are click here.

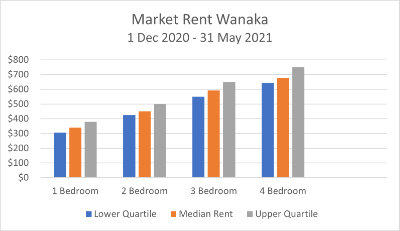

*Information sourced from Tenancy Services

Is a rental property in NZ an investor’s dream? Sure, the amount of rent that landlords are collecting in “hot spots” around the country is eye watering and very tempting if you have the 40% deposit now required to purchase an investment property (unless it is a new build). Add to this the new Bright Line Test rules which has altered an investor’s ability to offset interest paid on home loans against rental income (depreciation was removed in 2011), the period of time you need to keep the property increasing to 10 years for properties purchased after 27th March 2021 to avoid paying tax on capital gains (on resale) and don’t forget the increasing interest rates – phew …. you really need to sit down and look at the bottom line. I would like to point out that your primary home is exempt from the Bright Line Test but please do check with "specialists" around the rules for this.

What about AirBNB then ….. providing short-term accommodation can expose you to a variety of tax implications. As with any business, you can reduce the amount of tax that you are liable for by claiming any relevant expenses. The rules in this area are not straight-forward and we recommend you seek advice.

Having been a tenant, a home owner and a landlord I sympathise. Renting and trying to save enough deposit to buy is tough, coping with a mortgage is just as tough and navigating landlord obligations and at least breaking even is getting tougher. Mum and dad investors setting themselves up for retirement may need to consider their options.

My advice – seek expert advice. Talk to your tax specialist, your accountant, your local real estate salespeople and of course your local property manager. Understand the market and your obligations.

Thanks,

Jane Adams

Property Manager